Statistical Modeling for Communal Reserves: Financial Resilience

— by

Steven Haynes

Contents

1. Introduction: The hidden mechanics of resilience—why statistical modeling is the backbone of stable communal reserves.

2. Key Concepts: Understanding stochastic processes, buffer stocks, and the “Value at Risk” (VaR) framework in a communal context.

3. Step-by-Step Guide: Implementing a data-driven reserve management system.

4. Case Studies: Real-world applications in microfinance cooperatives and supply chain resilience.

5. Common Mistakes: Over-reliance on historical averages and ignoring “fat-tail” risks.

6. Advanced Tips: Utilizing Monte Carlo simulations and Bayesian updating for dynamic adjustment.

7. Conclusion: Moving from reactive to proactive reserve stewardship.

***

Statistical Modeling for Communal Reserves: Building Financial and Resource Resilience

Introduction

Whether in a local credit union, a communal grain store, or a decentralized digital autonomous organization (DAO), the challenge of sustainability remains the same: how do you maintain a reserve large enough to survive a crisis without stagnating the resources available for immediate growth? The answer rarely lies in intuition or “gut feeling.” It lies in the rigorous application of statistical modeling.

Communal reserves act as the shock absorbers for a collective. When those reserves are depleted, the community faces existential risk. When they are unnecessarily bloated, the community loses the opportunity to invest in its own development. Statistical modeling allows leaders to bridge this gap, transforming uncertainty into a quantifiable probability of survival. By shifting from static “rule-of-thumb” saving to dynamic, data-driven reserve management, communities can ensure they remain solvent, regardless of external economic or environmental volatility.

Key Concepts

To master communal reserves, you must first understand the mathematical landscape of risk. These three concepts form the foundation of any robust model:

1. Stochastic Processes: Unlike deterministic models that assume a steady, predictable flow of resources, stochastic modeling accounts for randomness. It acknowledges that withdrawals and deposits are not just numbers; they are variables subject to chance. By modeling these as probability distributions, we can predict a range of potential future states rather than a single, likely-to-be-wrong outcome.

2. Buffer Stock Theory: This concept posits that an optimal reserve level is reached when the marginal cost of holding an extra unit of reserve equals the expected marginal benefit of avoiding a stock-out. Statistical modeling identifies this “sweet spot,” preventing the inefficiency of over-accumulation while mitigating the danger of insolvency.

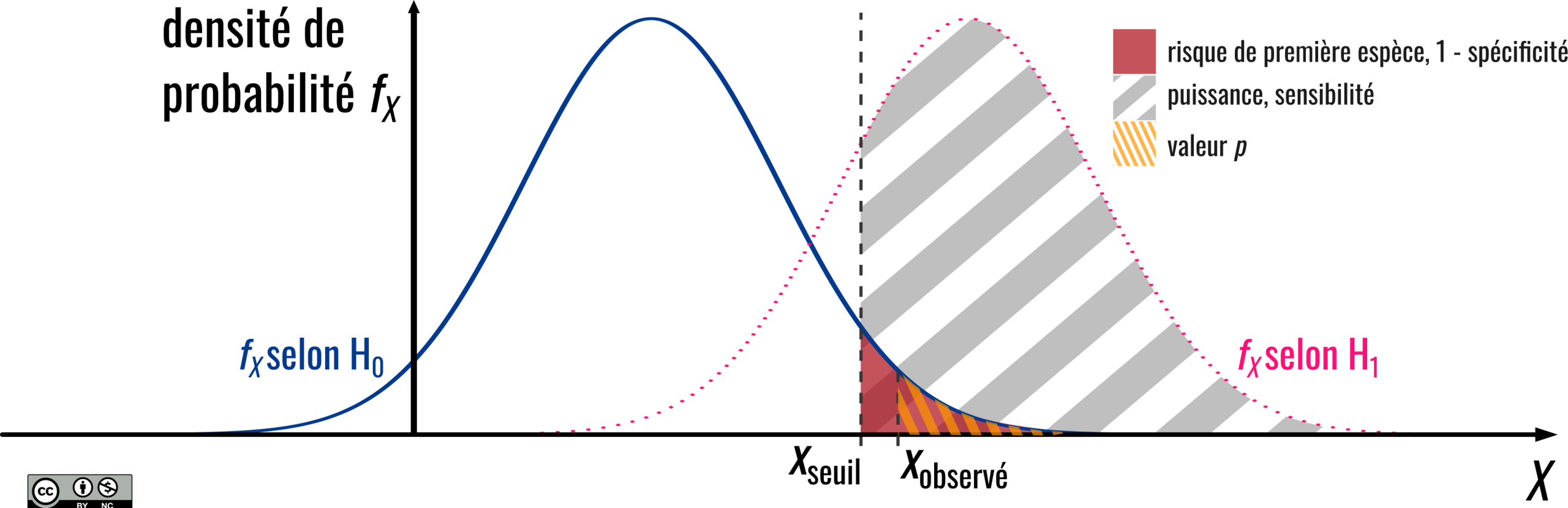

3. Value at Risk (VaR): Often used in finance, VaR is a statistical technique used to measure the level of financial risk within a firm or portfolio over a specific time frame. In a communal setting, it answers the critical question: “What is the maximum amount we are likely to lose, with a 95% or 99% confidence level, during a specific period?”

Step-by-Step Guide

Implementing a statistical model for your reserve management doesn’t require a PhD in mathematics, but it does require a disciplined approach to data. Follow these steps to build your system:

Data Collection and Cleaning: Aggregate at least 24 to 36 months of historical transaction data. Ensure you categorize inflows (deposits, yields) and outflows (withdrawals, emergency spending) separately. Remove outliers caused by one-time, non-repeating events to ensure the model reflects the “new normal.”

Define the Probability Distribution: Use your data to determine the distribution of your net cash flows. Most communal resource flows follow a “Normal” or “Log-Normal” distribution. If your community experiences high-frequency, small-scale shocks, a Poisson distribution may be more appropriate.

Set the Confidence Threshold: Decide on your “risk appetite.” A 95% confidence level implies you are comfortable with a 5% chance of the reserve dropping below a critical threshold. A 99% level is more conservative, requiring larger reserves but offering greater protection against “Black Swan” events.

Run Simulations: Use Monte Carlo simulations—a method that runs thousands of “what-if” scenarios based on your data—to determine the minimum reserve balance required to cover the outflows at your chosen confidence level.

Establish Dynamic Triggers: Your model should output a “Floor” and a “Ceiling.” If the reserve hits the Floor, automatic austerity measures or reserve-replenishment protocols must trigger. If it exceeds the Ceiling, surplus resources can be safely reallocated to communal projects.

Examples or Case Studies

The Microfinance Cooperative: A rural agricultural cooperative previously kept a flat 10% of total assets as a reserve. During a drought, this proved insufficient. By switching to a statistical model, they identified that their risk was correlated with local rainfall patterns. They adjusted their reserves to be higher during the planting season and lower after harvest. This “seasonal volatility adjustment” allowed them to keep more capital working in the community while actually increasing their protection against total collapse.

Supply Chain Resilience: A manufacturing collective used VaR modeling to manage their communal raw material reserve. They discovered that their lead times followed a skewed distribution. By modeling the “right tail” of the distribution—the rare but catastrophic long-delay events—they increased their safety stock specifically for high-risk components, reducing their overall inventory holding costs by 15% while improving their uptime.

Common Mistakes

Ignoring Correlation: A common error is assuming that all risks are independent. In a community, a shock often affects everyone simultaneously. If your model assumes individual failures are uncorrelated, you will drastically underestimate the size of the reserve needed to survive a systemic shock.

Recency Bias: Relying too heavily on the last six months of data. Statistical models require a long enough time horizon to capture the full cycle of economic or environmental volatility.

Static Thresholds: Setting a reserve level and forgetting it. If the community size, the market environment, or the risk profile changes, your model must be updated. A static model is a ticking time bomb.

Advanced Tips

To take your modeling to the next level, incorporate Bayesian Updating. This allows you to refine your model continuously as new data arrives. Instead of waiting for a year-end review, your reserve requirements can evolve quarterly or even monthly. If you see a trend of increasing withdrawal frequency, a Bayesian approach will automatically adjust the required reserve level upward, providing a proactive buffer before a crisis occurs.

“The goal of statistical modeling is not to predict the future with perfect accuracy, but to quantify the uncertainty of the future so that we can build systems that thrive despite it.”

Furthermore, consider Stress Testing. Once your model is built, intentionally feed it “broken” data: simulate a 30% drop in revenue combined with a 20% spike in withdrawals. If your current reserve model cannot survive that scenario, you have identified a vulnerability that needs to be addressed through insurance, credit lines, or increased member contributions.

Conclusion

Statistical modeling for communal reserves is the difference between a community that lives in constant fear of the next shock and a community that has mathematically engineered its own stability. By understanding the probability of your risks, collecting clean data, and running iterative simulations, you shift your management style from reactive panic to strategic confidence.

Start small: define your confidence threshold, analyze your historical volatility, and build your first “Floor.” As you gain comfort with the numbers, you will find that a well-managed reserve is not just a safety net—it is a powerful tool that enables your community to take calculated risks and pursue growth with the assurance that your foundation remains secure.

Leave a Reply